Disclaimer:

Any views expressed in the essay below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as advice or an advertisement to engage in any investment, service, strategy, or transaction.

Opening Remarks

The Federal Reserve pursues its dual mandate of price stability and maximum employment mainly by adjusting interest rates. At the April FOMC meeting, Jerome Powell used his final press conference as Chair to defend central bank independence. Facing political pressure, he announced he would remain on the Board of Governors after his term ends in May, rather than resign fully, until investigations conclude. This rare move (last seen with Marriner Eccles in 1948-1951) aims to protect the institution but also preserves a more balanced Board composition against further Republican influence. The FOMC voted 8-4 to hold the federal funds rate at 3.5%–3.75%, its third consecutive unchanged decision, highlighting deep divisions.

Markets now price in a modest chance of future hikes amid energy-driven supply shocks from the Iran conflict. Powell emphasized flexibility, but any move risks appearing political. Historical parallels to the 1992-1994 period suggest rates may stay steady before potential tightening, though today’s environment carries stagflation risks from rising unemployment, inflation, and slowing growth. Fiscal policy now dominates. Expansive spending and a $39 trillion national debt (plus $170 trillion in unfunded liabilities) pressure the Fed.

Observers anticipate a “Treasury-Fed Accord 2.0” under incoming Chair Kevin Warsh and Treasury Secretary Scott Bessent. This could involve structured swaps to normalize the Fed’s $6.71 trillion balance sheet while delivering lower short-term rates and hidden easing, supporting asset prices without market disruption. However, higher inflation from energy shocks could break this choreography, driving yields higher and recreating 1951-style tensions. Compared to the 1990s, today’s massive deficits (~6% of GDP) and debt (~122% of GDP) leaves less room for a soft landing. With default or austerity politically impossible, the likely path is currency debasement through liquidity and money creation.

In this environment, Bitcoin stands out as a prudent, non-debasable hedge with its fixed 21 million supply, offering protection against ongoing fiscal recklessness and monetary accommodation.

Central Bank Independence and the FOMC Decision

The Federal Reserve is the central bank of the United States tasked with a dual mandate by Congress of promoting stable prices and maximum employment. It pursues these goals mainly through monetary policy by adjusting interest rates to influence borrowing, spending, and inflation. Simply put, the Federal Reserve’s toolbox is more like a single tool, a screwdriver. When the economy slows and jobs are scarce, they loosen the economy by cutting rates, or, if the prices rise too fast, the Fed tightens up the economy by raising rates. The independence is granted by Congress to make these decisions based on data, and not political pressure.

On Wednesday, April 29, 2026, Jerome Powell answered questions about the FOMC’s policy rate decision and monetary policy at the press conference for his last time as chair of the Federal Reserve. This FOMC meeting was out of the ordinary with Powell breaking from his usual spiel making comments on central banking independence. In his view, the administration’s actions against the chair and Fed have left him no choice but to remain on the Board after his term as chair ends in May. Powell thinks the president’s criticism of the central bank puts the Fed’s ability to conduct monetary policy at risk saying that a Federal Reserve free of political influence is key. Rather than stepping away from the bank to pursue advisory roles and speaking gigs as is typical for Fed chairs after their term expires, Powell announced his decision to leave the Board once investigations cease and will continue to serve for a period that is yet to be determined.

In theory, central banks are designed to be independent that aims their actions towards the best interest of the public without any undue influence from any particular party or politician. Historically, most chairs have resigned from the Board entirely once their chairmanship ends, even though their term as governor might run longer. Powell’s choice is rare, but not unprecedented. The last time was Marriner Eccles, who stepped down as chair in January 1948 and continued to serve on the Board of Governors until 1951. The decision to stay by Jerome Powell is partly to protect the institution amid political pressure and ongoing investigations, but one could argue that his departure would mean Trump getting another nomination to the Board.

If Powell left after his term as Fed chair, Trump would be able to nominate a replacement governor to go along with his existing allies on the Board such as Michelle Bowman, Christopher Waller, and Stephen Miran. Powell leaving would give the administration another slot to fill with someone more aligned with its goals, shifting the balance of power at the Fed further towards the Republicans. The Fed has leaned towards the Democrats, but recently has become more split with the Republicans gaining an edge. The Federal Reserve has never purely been apolitical because presidents nominate the chair and who gets the long terms, but the Senate confirmation and staggered 14-year terms keeps any one administration from packing the Board.

Powell was never an economist; he has always been a political scientist and lawyer. It may seem that his decision to stay is noble, but it may be posturing. The best leverage he has is remaining on the Board until 2028 to keep the Federal Reserve Board’s alignment from shifting away from the Democratic Party. Under law, Powell understood that President Trump could not remove him or force his resignation and proclaimed such fact in a FOMC press conference when asked about such a possibility. It was one of the rare times the chair, soon to be former-chair, got flustered.

Monetary Policy

The Federal Reserve’s FOMC voted 8-4 to hold its benchmark rate in the 3.5% to 3.75% target range. The vote signals a highly divided Federal Reserve. It was the Fed’s third straight meeting leaving their Fed Funds rate unchanged. The Fed’s dissenting Governors were Hammack, Kashkari, and Logan voting against easing bias while Miran voted in favor of easing with a 25 basis-point rate cut. All in all, it was a highly unusual meeting and press conference for the Fed.

The last time there were four dissenting votes at an FOMC meeting was on October 6, 1992. Back at that time, the US was in a painfully slow “jobless” recovery after the 1990 recession that spilled into 1991. The majority at the 1992 meeting voted for more easing right away with two of the dissenters favoring stronger immediate action and the two others in favor of holding rates steady. In the year following this meeting, they held rates steady through 1993 before finally starting to raise them in February 1994. So, the big easing wave ended right around that October meeting in 1992.

Similar to 1993, the Federal Reserve may very well hold rates steady in 2026 before raising them next year like in 1994. It is important to understand what took place in 1994 when the Fed decided to hike its policy rate from 3% to 5.5% by year-end. As a result, the stock market went sideways as mortgage rates spiked and the long end of the yield curve for US Treasuries jumped from around 6.2% to 8%. The Federal Reserve’s classic policy-lag mismatch triggered the “Great Bond Massacre” of 1994 that was the worst bond market since 1927. In 2022, the Fed commit another policy-lag mismatch mistake following its rate hikes that caused a bond bear market that was bigger and took the crown in absolute dollar losses as well as market impact.

At Jerome Powell’s final FOMC press conference as Fed chair, he said that people are not saying they need to hike now and if needed they will certainly signal a rate hike. Powell posited that policy is in a good place to wait as well as move in either direction, depending on how things evolve in the next 30-60 days. He noted he has not seen the impact of higher prices yet, but that every supply shock can drive up unemployment as well as inflation in concern to the geopolitical tensions around the Iran War that is pushing energy prices higher in addition to gas prices, which means less disposable income for Americans that can be a drag on GDP. After holding rates higher-for-longer despite some cuts, there is talk of being “forced” to raise rates again with Fed swaps during the FOMC press conference pricing in a 50% probability of a 25-basis point rate hike by April 2027. Interest-rate futures after the closing bell show an 11% chance of a hike, up from 5% earlier Wednesday and 0% on Tuesday, while the odds of a rate cut sat around 2%.

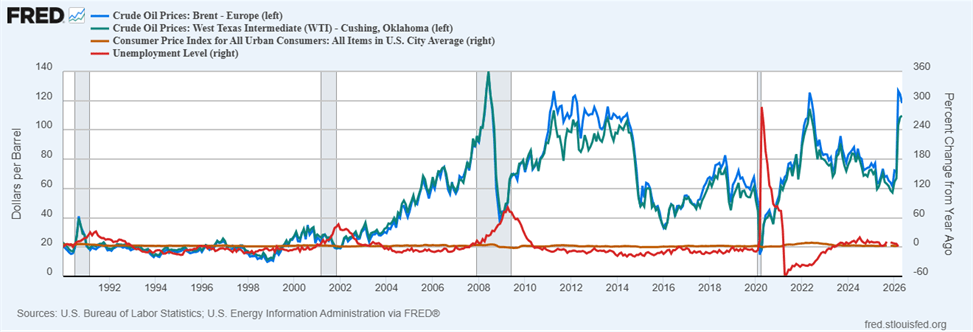

If the Federal Reserve cut rates, it may appear as if the central bank is being political and acting on the administration’s wishes. Or, if they raised rates, it may still seem adversarial and a form of political retribution against the administration’s wishes. Historically, supply shocks in energy have driven up the rate of inflation as well as the unemployment rate (appendix chart #1), putting the Fed’s monetary policy in a precarious position. They either risk raising rates into an energy shock that risks losing the long end of the yield curve or risk cutting rates into an energy shock that still risks losing the long end of the yield curve, looking politically motivated either way.

It can be expected that monetary policy will be subjugated into following fiscal policy going forward as the implications and importance of federal debt levels will dominate policymaking.

Fiscal Policy

The US Treasury is the executive department of the federal government responsible for managing the nation’s finances by collecting taxes through the IRS, issuing Treasury bonds to finance government borrowing, and overseeing the production of currency through the Bureau of Engraving and Printing. The Secretary of the Treasury serves as the principal economic advisor to the president and plays a central role in shaping fiscal policy, including decisions on debt levels, spending priorities, and international financial negotiations. While the Federal Reserve controls interest rates and the money supply, the Treasury controls how the government spends and borrows. Together, they form the backbone of the US economic power. However, their relationship is defined by careful separation and occasional tension.

John W. Snyder served as US Treasury Secretary from June 1946 to January 1953 under President Harry Truman. He strongly supported keeping interest rates artificially low, known as “the wartime peg,” to make government borrowing cheap and protect the value of war bonds, even as inflation surged in the years after the war ended. It was a stance that put him in direct conflict with the Federal Reserve. This led to a major feud with the Fed, and Marriner Eccles (who remained on the Board after his chairmanship ended) leaked the meeting to the press. His tactics forced negotiations where Eccles drew a hard line: the Federal Reserve would no longer be required to keep interest rates artificially low just to help the Treasury borrow cheap.

The 1951 Treasury-Fed Accord agreement led by Eccles freed the bond market and gave the Federal Reserve real independence to fight inflation rather than simply financing deficits. Today, they still coordinate closely with the Fed acting as the Treasury’s banker handling its debt auctions and managing the government’s cash account, but monetary policy remains legally distinct. The 1951 Accord established that the Fed is not obligated to finance government debts by artificially suppressing interest rates. That boundary is being tested again with Powell wrapping up as chair on May 15 while staying on as governor amid political pressure. With Kevin Warsh now about to take the helm of the Fed as its new chair, we are expected to be entering a Treasury-Fed Accord 2.0 between Treasury Secretary Scott Bessent and Warsh.

The expansionary fiscal stance currently adds demand pressure for US debt, potentially forcing the Fed’s hand on lowering interest rates while also pushing up long end yields through a heavier Treasury supply. This setup suggests lower short-term rates, a steeper yield curve, and an already deregulated banking sector that shifts the Fed’s balance sheet role to the private banks to “privatize” the Fed’s balance sheet. This maneuver will allow the Federal Reserve to appear as if it is tightening with a shrinking balance sheet while it is really continuing easing policy by warehousing the assets onto other private bank balance sheets. In effect, the policy will act as a hidden form of quantitative easing. As a result, asset prices and valuations will continue to rise.

As of April 22, 2026, the assets for all Federal Reserve Banks are roughly equivalent to $6.71 Trillion. Compared to 2026 federal spending that is over $7 Trillion and a national debt at $39 Trillion amid a rising deficit and increased spending under the current administration, the dominance of fiscal policy over monetary policy is proven by the numbers. In this scenario, inflation will prove to be persistently stubborn above target as a product of the government spending and borrowing. Owning assets that cannot be debased will protect investors from the fiscal recklessness and monetary madness that are set to continue without an end in sight.

Choreographed Fiscal and Monetary Policy

The Treasury-Fed Accord 2.0 could actually strengthen and redefine the “quantitative tightening for rate cuts” regime rather than undermine it. The idea of QT-for-rate-cuts was a workaround where the Fed would slowly shrink its balance sheet, which tends to push longer-term yields higher, while cutting short-term rates to offset the tightening effect and keep financial conditions easy. The Bessent-Warsh approach goes further. Instead of traditional quantitative tightening, where the Fed lets bonds roll off and sells assets that can tighten markets, they are talking about a structured swap. The Fed would transfer long-term Treasuries and MBS back to the Treasury, with the Treasury taking on the corresponding liabilities, such as excess reserves.

The choreographed policy would shrink the Fed’s footprint without dumping bonds into the market or creating a “taper tantrum.” In practice, this allows Warsh to lower short-term rates while normalizing the balance sheet more aggressively and cleanly. It removes the Fed’s distortion in long-term debt markets, which Warsh has called “fiscal policy in disguise,” while still giving the administration the easier financial conditions it wants. The bond market’s current quietness reflects investors’ expectations of a smooth coordinated handoff. If all goes to plan, it makes the QT-for-rate-cuts regime more sustainable.

The risk is that if inflation forces the Fed to raise rates instead of cutting them, the whole elegant coordination breaks down which risks breaking or severely straining the Bessent-Warsh Accord. The main point of their framework is coordinated easing, Warsh cuts short-term rates while the Fed shrinks the size of its balance sheet in a non-disruptive, organized manner with the Treasury. This setup relies on the Fed delivering lower rates to offset the upward pressure on long-term yields that comes with reducing its footprint. If inflation (CPI) that is currently projected at 3.7% for April is pushed higher by elevated oil and gas prices, the Fed’s policy rate will more likely be hiked and hamper the coordination from the Fed and Treasury for yield curve control. Higher short-term rates in addition to ongoing balance sheet normalization would drive both ends of the yield curve higher simultaneously, creating much tighter financial conditions than intended.

If inflation from the Iran War breaks down their choreography. The Treasury would face sharply higher borrowing costs on new debt, which Bessent would strongly oppose. Warsh, known for being tough on inflation, would likely prioritize fighting it rather than maintaining the smooth handoff. This recreates the exact tension that led to the original 1951 Accord, the Treasury wanting cheap financing for the government and the Fed refusing to subsidize it. A surprise shift to rate hikes would trigger a disorderly repricing, higher volatility, and pressure on the entire Accord framework. The markets seem to have priced in the smooth handoff, so a flare up in inflation may have serious ramifications on the feasibility of a Treasury-Fed Accord 2.0.

The similarities to the 1990s and today are striking in the monetary setup, but the fiscal policy is where the script flips. Fiscal policy makes this time different, and riskier. In the mid-1990s, Clinton pushed serious deficit reductions that helped bring down long-term rates and supported a soft landing. Right now in 2026, the US is running massive deficits, around $1.9 Trillion or nearly 6% of GDP, with debt sticking around 122% of GDP versus around 61% in 1992 (see appendix chart #2). The 1994 playbook worked partly because the fiscal policy helped share the load, but that is not as convenient today and tightening risks a sharper mismatch as well as a bigger market tantrum.

Final Thoughts

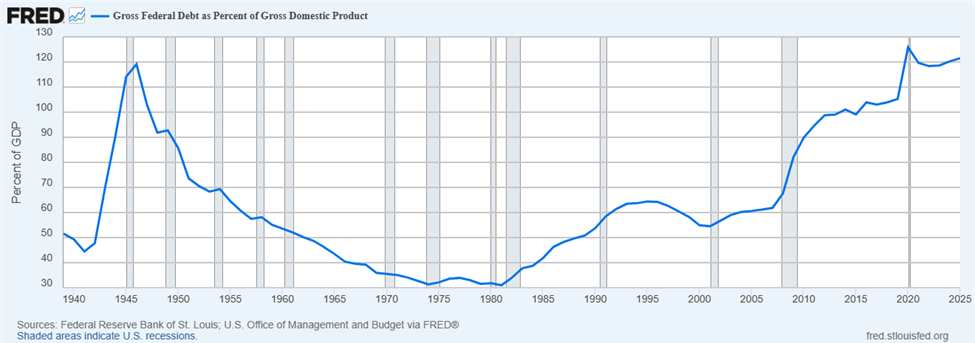

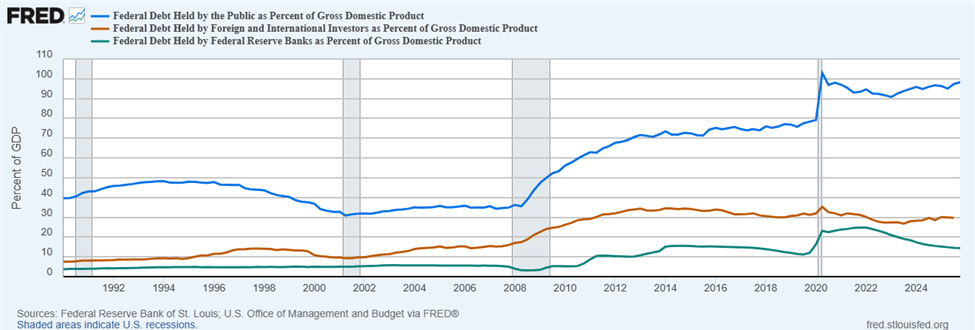

According to the US Office of Management and Budget, the gross federal debt as a percent of gross domestic product (GDP) is higher today than it was at its peak after WWII (see chart #2 in the appendix). Since 1994 (on appendix chart #3), the federal debt held by the public as a percent has increased to roughly 100% of GDP while federal debt held by Federal Reserve Banks (green) as a percent of GDP at about 14% has broadly trended higher along with federal debt held by Foreign and International Investors (orange) as a percent of GDP at about 30%. After Janet Yellen as Treasury Secretary effectively canceled and seized Russia’s US Treasuries, foreign and international investors who were likely surprised by the move have seemed to pause their buying of US debt along with the Federal Reserve Banks that were tasked with quantitative tightening and shrunk their holdings as a percent of GDP since 2022. If the Federal Reserve raises interest rates, it may spur another bond market catastrophe with yields rising and prices falling that impairs their value on bank balance sheets, thus constraining lending and therefore financial liquidity. As the “lender of last resort,” that is where the Federal Reserve steps in.

The United States has taken deep pride in the United States Dollar as the world’s reserve currency that is backed by the full faith and credit of the US government. In 2011 on Meet the Press, right after the S&P downgraded the credit rating for US debt, the former Federal Reserve chair from 1987 to 2006 Alan Greenspan proclaimed, “The United States can pay any debt it has because we can always print money to do that. So there is zero probability of default.” He meant that an actual default is impossible for a country that issues its own currency that is held and regarded as the world’s reserve currency. In a bond market collapse, the Fed can simply step in to print the money to buy the bonds back, making investors whole. Easy peasy lemon squeezy.

A major difference in Marriner Eccles’s decision to remain on the Board of Governors at the Federal Reserve after his term as chair expired compared to Jerome Powell’s is that President Truman expressly asked him to stay as opposed to Trump who has vehemently requested Powell to step down and away from the central bank. Many economists would argue that Powell staying at the Fed is a political move, but it also could be good for optics for his legacy after being compared to Arthur Burns for much of his second term as chair of the Fed. Burns, Fed chair from 1970 to 1978, is highly regarded as the worst chair of the Federal Reserve due to his role in the “Great Inflation” of the 1970s. His tenure was marked by political pressure from President Nixon, which led to overly accommodative monetary policies to curb inflation. Burns favored low interest rates and high monetary growth to promote employment and wrongly believed inflation was caused by factors other than money supply (like oil shocks or wages), blaming labor unions or idiosyncratic factors rather than managing monetary policy appropriately.

Given that energy prices have soared since the beginning of the operation in Iran and Strait of Hormuz, it would not be entirely out of order for the Federal Reserve to cut rather than hike rates. In the 1990s, Middle East oil price increases spurred rate cuts by Alan Greenspan in addition to an emergency rate cut decision meeting post-9/11 with a 50 basis-point cut. It would mean they abandon their stable prices mandate for 2% inflation and blame their maximum employment mandate forcing them to lower rates with a rising unemployment rate. Companies in COVID were incentivized by the government not to layoff employees due to the PPP loans, and post-COVID many of the same companies have found artificial intelligence (AI) tools make employees more productive, and redundant. With a lack of subsidization and AI as a convenient excuse to cut headcounts, the unemployment rate rising along with inflation and slowing growth due to the higher energy prices altogether create a rare economic condition called “stagflation.”

President Trump, like any politician, campaigned on promises that he could not deliver on. Namely, lowering the deficit and national debt. All of the Department of Government Efficiency (DOGE) efforts have been for nothing. The $39 trillion national debt does not fully account for the unfunded line items for defense, Medicare, social security, federal pensions, veterans, and other liabilities totaling $170 trillion. This leaves the US trapped in a debt spiral without a politically viable path out rather than currency debasement (printing or inflating away the real value of obligations). All politicians will resort to the easy path, printing, rather than soberness.

Default or drastic austerity are off the table, so the Treasury and Fed will rely on liquidity, quantitative easing, and money creation that all erode the dollar’s purchasing power over time. US Treasuries are no longer the safe diversifier in portfolios that are ultimately risky rather than “risk-free” due to printing, and gold is not as finite or provably scarce or secure as Bitcoin. Bitcoin as a non-debasable digital property with its fixed 21 million supply is “the best inflation hedge,” according to the legendary investor Paul Tudor Jones. Liquidity cycles, Fed policy, and deficits fuel Bitcoin’s price and investors expect that its outperformance continues as debasement accelerates. With the $200 trillion US debt reality in mind, Bitcoin as an investment is no longer as speculative as it is prudent risk management. It is a lifeboat in a system forced to inflate.

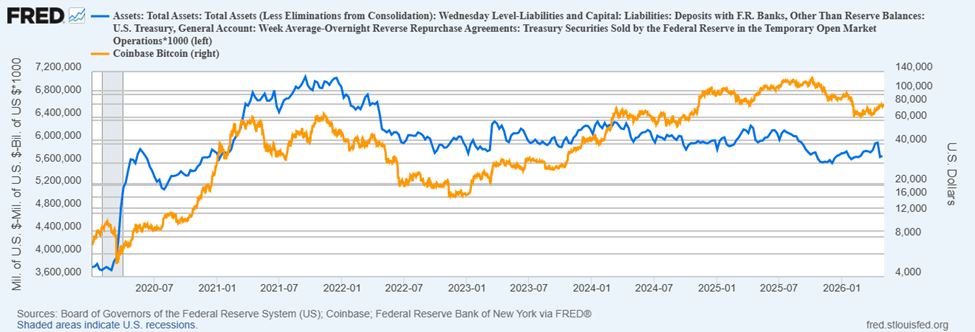

Since 2020 (as seen on appendix chart #4), Bitcoin (orange line) has been tracking the proprietary US Dollar Liquidity Index (blue line) that measures domestic financial liquidity conditions by taking the Total Assets on the Fed’s balance sheet minus the Treasury’s General Account (TGA) at the Fed minus Overnight Reverse Repo agreements (RRP). The TGA typically rises during periods of high tax receipts (especially around April 15) and immediately following debt ceiling increases, when the Treasury issues large amounts of new debt. TGA balances also rise when the Treasury builds a cash buffer to manage potential fiscal uncertainties or government shutdowns. The Fed’s RRP facility usage generally rises when there is an excess of liquidity (cash) in the financial system and a shortage of safe, short-term investment options like Treasury bills, so money market funds (MMFs) turn to the Fed to securely park excess cash.

A successful Treasury-Fed Accord 2.0 would deliver net positive effects on domestic liquidity conditions by creating the appearance of monetary tightening while actually sustaining or expanding easing through coordinated balance sheet engineering. Under the structured swap mechanism, it allows the Fed’s $6.71 trillion balance sheet to shrink without selling assets into the open market that avoids a sharp spike in long-term yields. At the same time, Kevin Warsh would cut short-term policy rates to deliver easier financial conditions. The key liquidity transmission occurs through “privatization” of the Fed’s balance sheet. By warehousing the transferred assets onto private bank balance sheets, the arrangement keeps associated reserves and liquidity circulating within the domestic financial system rather than draining it.

The Bessent-Warsh Accord functions as hidden quantitative easing where the Fed appears to be normalizing its balance sheet while maintaining tightening optics, yet the overall liquidity available to banks, borrowers, and markets remains ample and/or grows. Lower short-term rates reduce funding costs and encourage credit creation by banks. Reduced RRP facility usage (as excess cash finds better private-sector outlets) or declining TGA balances (depending on Treasury issuance timing) would support a higher reading on the US Dollar Liquidity Index. A steeper yield curve (low front-end, contained long-end) boosts bank net interest margins and profits that incentivizes lending. Without a disorderly bond sell-off, it preserves confidence in collateral values and supports repo markets as well as the functioning of overall money-markets.

In a nutshell, the successful handoff and implementation of the Treasury-Fed Accord 2.0 would loosen domestic liquidity conditions despite the Fed footprint shrinking. This sustains easy financial conditions, supports asset prices, and aligns with the expansionary fiscal stance and ongoing deficits. The result reinforces currency debasement pressures, as the system prioritizes liquidity provisioning over genuine tightening. As a non-debasable asset and hedge against inflation, this favors Bitcoin in a world of expanding deficits, stubbornly high inflation, and Fed-Treasury coordinated easing. Its correlation to liquidity strengthens Bitcoin’s role as a prudent hedge, making investment in it less of a gamble and more of structural risk management against currency erosion. It explains its growing adoption by banks, corporations, and nation-states.

Appendix Charts

Chart #1

Chart #2

Chart #3

Chart #4